They form a chain connecting them all. Because the chain cannot be removed or altered without network approval, the data is constant across time. Thus, you may monitor orders, payments, accounts, and other transactions by creating an unchangeable or immutable ledger using blockchain technology. Unauthorized transaction inputs are prevented by built-in system features, which also ensure consistency in the common view of these transactions.

Why does blockchain matter?

There are several obstacles when it comes to capturing financial transactions using traditional database technology. Take the selling of a property, for example. Ownership of the property passes to the buyer once payment exchanged. Both the seller and the buyer can independently record the financial transactions, but neither source is reliable. Both the buyer and the seller might easily argue that they have paid the money even if they haven't gotten it, or that they haven't received it as all.

Transactions must be supervised and validated by a reliable third party to prevent possible legal problems. In addition to making the transaction more difficult, the existence of this central authority adds one more point of risk. If there was a breach in the central database, both sides may be affected.

Blockchain reduces these problems by establishing a decentralized, impenetrable transaction record system. Within the real estate transaction context, blockchain generates a single ledger for both the vendor and the buyer. Every transaction is immediately updated in real time in both parties' ledgers and requires approval from both parties. The whole ledger will become tainted if there is any corruption in past transactions. Due to these characteristics, blockchain technology is being used in a number of industries, including the production of virtual currencies like Bitcoin.

What applications does blockchain have across industries?

Blockchain is a new technology that many different sectors are embracing creatively. We go over a few application scenarios across several sectors in the subsections that follow:

Vitality

Blockchain technology is being used by energy firms to provide peer-to-peer energy trading systems and to simplify the process of obtaining renewable energy. Take these applications, for instance:

Energy businesses that use blockchain technology have developed a marketplace where people can buy and sell electricity to each other. Using this platform, solar-paneling homeowners may sell their extra solar energy to nearby residents. The majority of the procedure is automated: blockchain records the transactions that smart meters produce.

Users in places without access to electricity may sponsor and own solar panels through crowd fundraising projects based on blockchain technology. After the solar panels are built, sponsors may also get rent for these neighborhoods.

Money

Blockchain services are used by established financial institutions, including as banks and stock exchanges, to handle online payments, accounts, and market trading. For instance, blockchain technology is being used by Singapore Exchange Limited, an investment holding firm that offers financial trading services across Asia, to create an interbank payment account that is more effective. They overcame a number of obstacles by using blockchain, such as batch processing and the laborious manual reconciliation of thousands of financial transactions.

Entertainment and media

Blockchain technologies are used by media and entertainment companies to handle copyright data. Verifying copyright is essential to paying artists fairly. To document the sale or transfer of copyrighted content, many transactions are required. Blockchain services are used by Sony Music Entertainment Japan to improve the effectiveness of digital rights management. They have effectively reduced expenses and increased productivity in copyright processing by utilizing the blockchain technique.

Shop

Blockchain technology is used by retail businesses to monitor the flow of goods between suppliers and customers. For instance, Amazon Retail has submitted a patent application for a distributed ledger technology system that would make use of blockchain technology to confirm the authenticity of every item sold on the platform. By enabling parties like manufacturers, couriers, distributors, end users, and secondary users to contribute events to the ledger after enrolling with a certificate authority, Amazon merchants may trace their worldwide supply chains.

What characteristics does blockchain technology have?

The following are the key characteristics of blockchain technology:

Dispersion

In the context of blockchain, decentralization is the process of shifting power and decision-making from a centralized entity—a person, an organization, or a group—to a dispersed network. Transparency is used by decentralized blockchain networks to lessen the requirement for participant confidence. Additionally, these networks discourage users from abusing their power or dominance over one another in ways that impair the network's performance.

Unchangeability

Something is said to be immutable if it cannot be modified. Once a transaction has been entered into the shared ledger, nobody else can alter it. In the event that a transaction record has an error, the error must be corrected by adding a new transaction, and the network can see both transactions.

Accord

Rules about participant consent are established by a blockchain system in order to record transactions. Only when the approval of the majority of network members is obtained can new transactions be recorded.

Which fundamental elements make up blockchain technology?

The following are the primary elements of blockchain architecture:

A dispersed ledger

The shared database in the blockchain network that houses the transactions is called a distributed ledger; it may be thought of as a shared file that all team members can modify. Anybody with editing permissions may erase the whole file in the majority of shared text editors. Distributed ledger solutions, however, have tight guidelines regarding who may and cannot update. Once an entry has been recorded, it cannot be removed.

Intelligent contracts

Smart contracts allow businesses to self-manage contracts without the help of a third party. These are apps that are kept on the blockchain and activate automatically in response to specific events. To ensure that transactions can be finished with confidence, they perform if-then checks. A smart contract may be set up by a logistics business, for instance, to pay the supplier immediately as soon as the goods reach the port.

Cryptography Using Public Keys

One security component that allows users to be individually identified inside a blockchain network is public key cryptography. For each member of the network, this process creates two sets of keys. A single key is a public key that is shared by all network users. The other is an individual private key for each participant. Together, the public and private keys enable the ledger's data to be unlocked.

John and Jill, for instance, are two individuals within the network. John uses his private key to encrypt a transaction that he records. Jill's public key will allow her to decode it. Jill is convinced that John completed the transaction in this way. If John's private key had been compromised, Jill's public key would not have functioned.

How is blockchain technology implemented?

The following stages provide a quick summary of the intricate blockchain mechanics. Most of these stages can be automated by blockchain software:

Step 1: Keep a record of the exchange

A blockchain transaction documents the transfer of digital or tangible assets between participants in the network. It is stored as a block of data and may contain information similar to this:

-

Who took part in the exchange?

-

What took place in the course of the transaction?

-

When was the transaction completed?

-

Where was the transaction done?

-

Why was the transaction made?

-

What portion of the asset was traded?

How many prerequisites were satisfied throughout the course of the deal?

Step 2: Reach an understanding

The majority of users on the distributed blockchain network must concur that the transaction that was recorded is legitimate. Rules of agreement might differ depending on the kind of network, but they are usually set up from the outset.

Step3: Connect the blocks

Transactions on the blockchain are recorded into blocks, which are like to the pages of a ledger book, once the participants have come to an agreement. A cryptographic hash is applied to the new block along with the transactions. The blocks are connected by the hash, which functions as a chain. The hash value varies in response to purposeful or inadvertent modifications of the block's contents, offering a means of identifying data tampering.

As a result, the chains and blocks link safely and are not editable. Every new block reinforces the prior block's verification, strengthening the chain as a whole. It's similar to building a skyscraper out of wooden blocks. Only blocks may be stacked on top of one another, and the tower collapses as a whole if a block is taken out of the center.

Step4: Distribute the ledger

Every participant receives a copy of the most recent central ledger via the system.

Which kinds of blockchain networks exist?

The blockchain has four primary categories of distributed or decentralized networks:

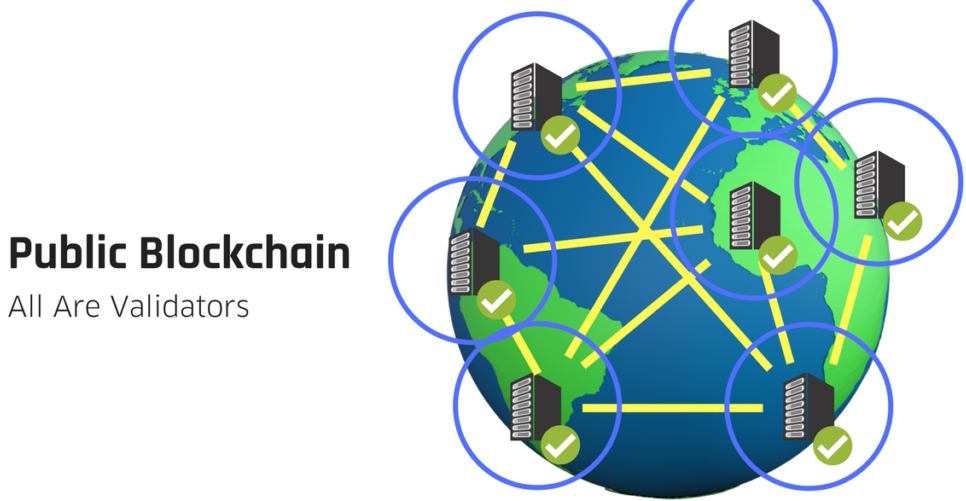

Networks For Public Blockchains

Public blockchains are open to all users and are permissionless. Each and every blockchain participant is entitled to view, amend, and validate the blockchain. The main uses of public blockchains are for mining and trading of cryptocurrencies such as Litecoin, Ethereum, and Bitcoin. You may alos read this: Successful Metaverse Real Estate Investing

Networks Of Private Blockchains

Private blockchains, also known as controlled blockchains, are under the control of a single entity. Who may join the network and what privileges they have are decided by the authorities. Due to access limitations, private blockchains are only partially decentralized. One example of a private blockchain is the digital currency exchange network for businesses called Ripple.

Blockchain Networks That Are Hybrid

Blockchains that are hybrids incorporate components from public and private networks. Businesses can install permission-based private systems in addition to public ones. They maintain public access to the other data while controlling access to certain data contained in the blockchain. They let members of the public verify if private transactions have been finished through the use of smart contracts. Hybrid blockchains, for instance, can allow the public to access digital cash while maintaining the privacy of bank-owned currency.

Blockchain Networks In Consortiums

Consortium blockchain networks are governed by a collection of organizations. Pre-selected entities are equally accountable for data access rights determination and blockchain maintenance. Consortium blockchain networks are typically preferred in industries where a large number of firms share same aims and benefit from shared accountability. One non-profit blockchain group that attempts to improve cooperation amongst marine industry operators and modernize the shipping sector is the Global Shipping Business Network group.

What advantages does blockchain technology offer?

Asset transaction management benefits greatly from blockchain technology. Several of them are enumerated in the subsequent subsections:

Enhanced security

The high degree of trust and security needed for contemporary digital transactions is offered by blockchain technologies. The constant worry is that someone may tamper with the underlying software to make fraudulent money for themselves. But blockchain creates an extremely secure underlying software system that is almost hard to tamper with by utilizing the three concepts of encryption, decentralization, and consensus. The transaction records cannot be altered by a single user, and there is no single point of failure.

Enhanced effectiveness

Business-to-business transactions can be laborious and lead to operational delays, particularly when third-party regulatory agencies and compliance are involved. These commercial interactions are made quicker and more effective by blockchain's transparency and smart contracts.

Quicker auditing

Businesses need to be able to create, trade, store, and reassemble e-transactions in an auditable way while maintaining security. Since blockchain data is unchangeable chronologically, all records are always arranged chronologically. Due to the openness of the data, audit processing is accelerated.

What distinguishes blockchain technology from Bitcoin?

Although the terms blockchain and bitcoin are sometimes used synonymously, they are not the same. Because Bitcoin was one of the first applications of blockchain technology, this misconception was unintentionally created when individuals started using Bitcoin to refer to blockchain. However, blockchain technology is not just for Bitcoin.

One digital currency that runs decentralized is called Bitcoin. Although they were first developed to facilitate online financial transactions, bitcoins are today regarded as digital assets that may be exchanged for any other major world currency, such as the US dollar or the euro. The primary ledger of Bitcoin is created and maintained via a public blockchain network.

Bitcoin network

All Bitcoin transactions are kept on a public ledger, copies of which are stored on servers throughout the globe. The servers resemble financial institutions. While individual banks are only aware of the money their clients exchange, Bitcoin servers are aware of every Bitcoin transaction that takes place worldwide.

A node is one of these servers that may be set up by anybody with an extra computer. It's similar to creating a Bitcoin bank as opposed to a traditional bank account.

Mining Bitcoins

Members mine for bitcoin on the open Bitcoin network by resolving mathematical puzzles to produce new blocks. Every new transaction is shared from node to node throughout the network by the system, which broadcasts it publicly. Miners gather these transactions into a fresh block every 10 minutes or so, adding them permanently to the blockchain—which serves as Bitcoin's official ledger.

Because mining involves a complicated software process, it takes a long time and a lot of computer resources. Miners receive a little quantity of bitcoin in return. The miners log transactions and gather transaction fees in a manner akin to that of contemporary clerks.

With blockchain cryptography, all network users come to an agreement on who is in possession of whose currency.

What distinguishes a blockchain from a database?

A unique kind of database management system called blockchain offers more functionalities than a standard database. The following list outlines some key distinctions between a blockchain and a regular database:

-

Blockchains distribute power without undermining current data's credibility. Other database systems do not permit this.

-

Businesses engaged in a transaction are unable to reveal their whole database. However, with blockchain networks, every business has a duplicate ledger, and the technology automatically keeps the two ledgers consistent.

-

Blockchain only allows for data insertion; in contrast, conventional database systems allow for data editing and deletion.

What distinguishes blockchain from the cloud?

Online-accessible computer services are referred to as cloud computing. Cloud-based services include Infrastructure as a Service (IaaS), Product as a Service (PaaS), and Software as a Service (SaaS). Through the internet, cloud providers let you access to their hardware and infrastructure for management purposes. Beyond database administration, they provide a plethora of other services. In order to participate in a public blockchain network, you will need to supply the hardware necessary to maintain a copy of your ledger. For this, you may also utilize a cloud-based server. Complete Blockchain as a Service (BaaS) is another service that certain cloud providers provide.

Blockchain as a Service: What Is It?

Blockchain as a Service (BaaS) is a cloud-based managed blockchain service offered by a third party. With the infrastructure and blockchain construction tools provided by the cloud provider, you may create blockchain apps and digital services. To accelerate and improve the efficiency of blockchain adoption, all you need to do is modify currently available blockchain technology.